As the leader of a real estate team and as a coach I often work with newer Realtors®

One of the first exercises I take them through in office (we just did this the other day with our 2 young Realtors® on the team) is a goal-setting exercise where they give voice to their desired “hourly rate” in the first years of their career.

Often times if prefaced correctly they will come up with things that are anywhere from reasonable to a bit ambitious, but that’s a good thing! (Because if they are ambitious you can work backwards into what it will take to achieve their goals.

But if you can imagine - someone coming from a $30-$50k annual job working 2,000 hours per year, they will set value exchange at things like $35-$50 p/h year one - $50-$100 year two, etc.

In the next part of the exercise, I talk about what it will take “each year” to stay on track and some of the pitfalls I’ve observed in my 20+ years working with Realtors / sales professionals, and now working as an owner of a local real estate business these past 5 years.

The staying on track part is straightforward - if you don’t put in the effort you commit to each year, you will fall behind in your timeline and there is a greater than 1-1 ratio (put in 20% less effort in year one, you’re going to be more than 20% behind in year two as you are not compounding your knowledge, practice, and ability.

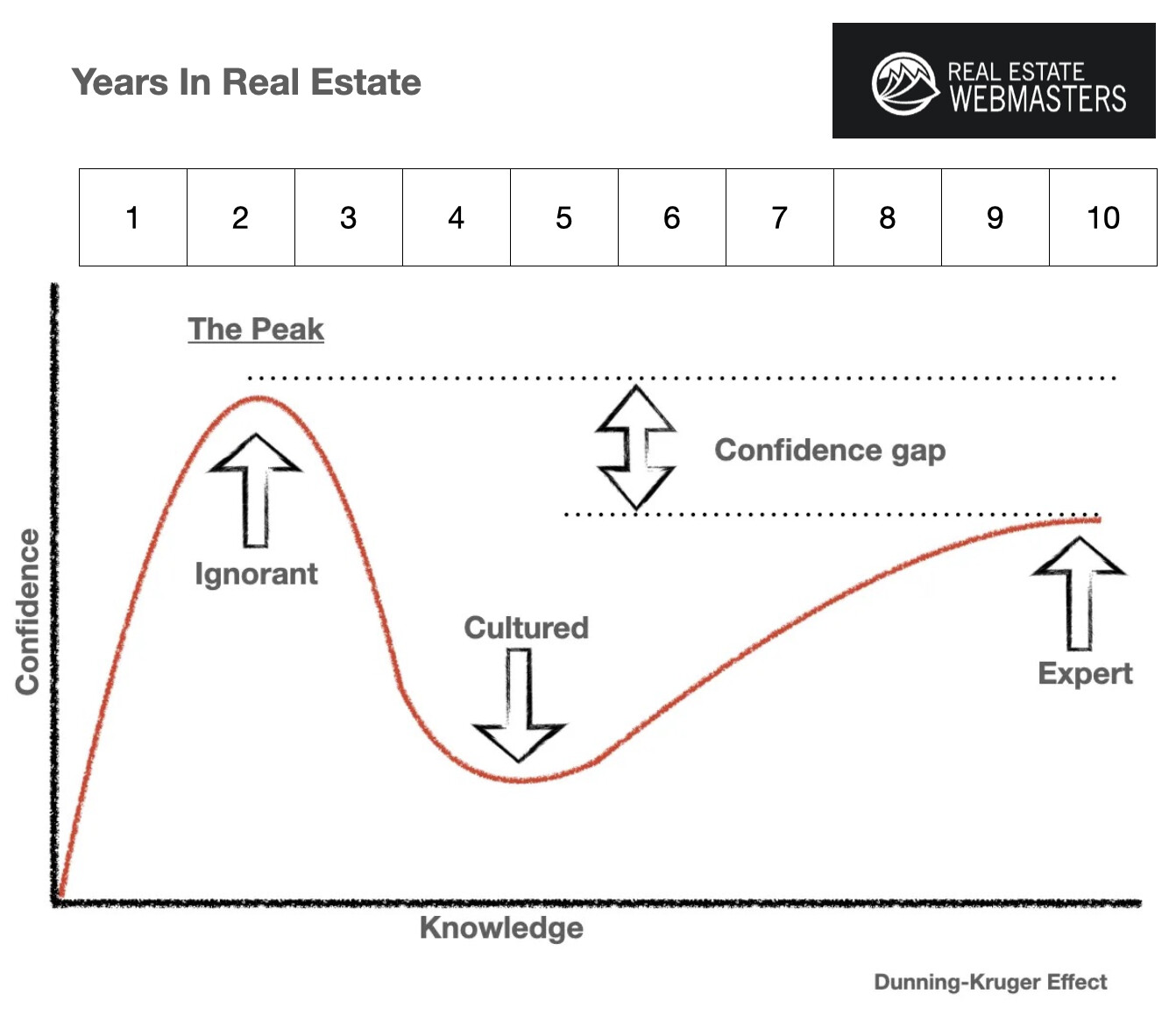

The part that I often struggle the most with (and admittedly this is typically with younger people as they have less life experience and perhaps have not learned this in other careers) is the uncomfortable period of the first few years where their knowledge “compared to” the fact that they knew zero before grows quite quickly. Thus they become overconfident in their abilities.

It’s a hard thing to get agents to believe if they have no lived it yet, however, it is something we all go through.

Recently I was listening to Neil Degrasse and he turned me onto a model that actually articulates this very well and it is referred to as the Dunning-Kruger Effect.

The graph below demonstrates this effect and I have added a timeline for my team so that they can understand the model in the context of their careers and we can have a fulsome discussion.

A few points I want to emphasize for the newer Realtors®

#1: There is absolutely nothing wrong or unnatural about where you are in the curve. The purpose of this exercise is to help you understand where you are and where you will be in the future.

#2: Understanding where you are in the curve, will help you interact with others and adjust your confidence output. (Being overconfident with a lack of knowledge/expertise is a turn-off and can harm your credibility)

#3: Knowing where you are in the curve helps you understand just how much growth potential (in both knowledge and earnings) you have ahead of you.

And at the end, I want to remind them - that there is an inverse relationship between how hard they work (or feel they have to work) vs their earnings as they go through this curve.

Experts “Make it look easy” (and candidly, it is MUCH easier to navigate transactions, attract more business and earn more money “in less time” once you’ve mastered your craft)

So if you feel like you’re killing yourself working 60-80 hours a week to close 2 deals a month but in the future you want to close 6 deals a month - don’t do “the thing” where you think you have to work 3x harder (and put in 3x more time) - what you need is 6x more knowledge (to become an expert) and you’ll find you can actually do 3x more deals in 2/3 the time.

It’s a bright future if you focus on developing your knowledge. Hope this graph helps ![]()